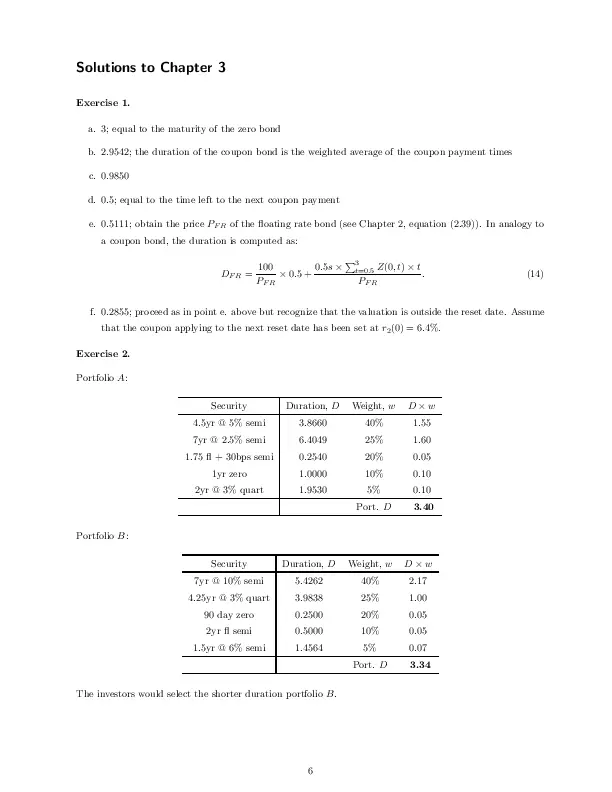

Solutions to Chapter 3

Exercise 1.

a. 3; equal to the maturity of the zero bond

b. 2.9542; the duration of the coupon bond is the weighted average of the coupon payment times

c. 0.9850

d. 0.5; equal to the time left to the next coupon payment

e. 0.5111; obtain the price PF R of the floating rate bond (see Chapter 2, equation (2.39)). In analogy to

a coupon bond, the duration is computed as:

0.5s ×

100

× 0.5 +

DF R =

PF R

P3

t=0.5 Z(0, t) × t

PF R

.

(14)

f. 0.2855; proceed as in point e. above but recognize that the valuation is outside the reset date. Assume

that the coupon applying to the next reset date has been set at r2 (0) = 6.4%.

Exercise 2.

Portfolio A:

Security

Duration, D

Weight, w

D×w

4.5yr @ 5% semi

3.8660

40%

1.55

7yr @ 2.5% semi

6.4049

25%

1.60

1.75 fl + 30bps semi

0.2540

20%

0.05

1yr zero

1.0000

10%

0.10

2yr @ 3% quart

1.9530

5%

0.10

Port. D

3.40

Portfolio B:

Security

Duration, D

Weight, w

D×w

7yr @ 10% semi

5.4262

40%

2.17

4.25yr @ 3% quart

3.9838

25%

1.00

90 day zero

0.2500

20%

0.05

2yr fl semi

0.5000

10%

0.05

1.5yr @ 6% semi

1.4564

5%

0.07

Port. D

3.34

The investors would select the shorter duration portfolio B.

6

Exercise 3.

Obtain yield to maturity y for each security. Compute modified and Macaulay duration accodring to equation

(3.19) and (3.20) in the book.

Yield

Duration

Modified

Macaulay

a.

6.95%

3

3

2.8993

b.

6.28%

2.9542

2.9974

2.9061

c.

6.66%

0.9850

0.9850

0.9689

d.

0.00%

0.5

0.5

0.5

e.

6.82%

0.5111

0.5111

0.4943

f.

6.76%

0.2855

0.2855

0.2761

Exercise 4.

Compute the duration of each asset and use the fact that the dollar duration is the bond price times its

duration.

Price

Duration

$ Duration

a.

$89.56

4.55

$407.88

b.

$67.63

-7.00

($473.39)

c.

$79.46

3.50

$277.74

d.

$100.00

0.5

$50.00

e.

$100.00

-0.25

($25.00)

f.

$102.70

-0.2763

($28.38)

Exercise 5.

a. Compute number of units of each security (N ) in the portfolio and apply Fact 3.5.

Portfolio A:

Security

Price

Duration

Weight

N

D×P ×N

4.5yr @ 5% semi

94.03

3.8660

40%

0.43

154.64

7yr @ 2.5% semi

81.56

6.4049

25%

0.307

160.12

1.75 fl + 30bps semi

102.09

0.2540

20%

0.20

5.08

1yr zero

93.61

1.0000

10%

0.11

10.00

2yr @ 3% quart

92.54

1.9530

5%

0.05

9.76

$D

339.61

7

Portfolio B :

Security

Price

Duration

Weight

N

D×P ×N

7yr @ 10% semi

123.36

5.4262

40%

0.32

217.05

4.25yr @ 3% quart

86.83

3.9838

25%

0.29

99.59

90 day zero

98.45

0.2500

20%

0.20

5.00

2yr fl semi

100.00

0.5000

10%

0.10

5.00

1.5yr @ 6% semi

98.83

1.4564

5%

0.05

7.28

$D

333.92

b. For 1 bps increase, we have (see Definition 3.5):

Portfolio A: 339.61 × 0.01/100 = −$0.0340

Portfolio B: 333.92 × 0.01/100 = −$0.0334

c. Yes.

Exercise 6.

After the reshuffling of the portfolio, its value becomes $50 mn.

a. Short -0.307 units of long bond in portfolio A, and -0.081 units in portfolio B.

b. New dollar durations are: 19.36 and 62.61 for portfolio A and B, respectively.

c. The conclusion reverses.

N LT bond

New weight LT bond

New $D

Port. A

-0.307

-25%

19.36

Port. B

-0.081

-10%

62.61

Exercise 7.

a. $10 mn

b. Compute the dollar duration of the cash flows in each bond, and then the dollar duration of the

portfolio:

Security

Position

$ (mn)

Price

N

$D

$D × N

6yr IF @ 20% – fl quart

Long

20.00

146.48

0.137

1,140.28

155.69

4yr fl 45bps semi

Long

20.00

101.62

0.197

53.54

10.54

5yr zero

Short

(30.00)

76.41

-0.393

382.052

-150.00

Port. value

$10.00 mn

Port. $D

16.23

Exercise 8.

a. The price of the 3yr @ 5% semi bond is $97.82. You want the duration of the hedged portfolio to be

zero. You need to short 0.058 units of the 3-year bond, i.e. the short position is -$5.69.

8

b. The total value of the portfolio is: $4.31 mn.

Exerxise 9.

Compute the new value of the portfolio assuming the term structure of interest rates as of May 15, 1994.

Original

Now

∆ value

Unhedged port.

$10.00

$8.97

($1.03)

Hedge

($5.69)

($5.44)

$0.25

Total

$4.31

$3.53

($0.78)

a. $8.97 mn

b. $3.53 mn

c. The immunization covered part of the loss. The change in the value of the portfolio is both due to (i)

the passage of time (coupon) and (ii) the increase in interest rates.

Exercise 10.

Use the curve given on May 15, 1994, but keep the times to maturity unchanged from the initial ones. The

change in value is due to the change in interest rates only.

Original

Now

∆ value

Unhedged port.

$10.00

$9.97

($0.03)

Hedge

($5.69)

($5.43)

$0.26

Total

$4.31

$4.54

$0.23

Exercise 11.

Use the curve given on February 15, 1994, but change the times to maturity to those on May 15, 1994. The

change in value is due to coupon only.

Original

Now

∆ value

Unhedged port.

$10.00

$9.12

($0.88)

Hedge

($5.69)

($5.68)

$0.01

Total

$4.31

$3.45

($0.87)

Exercise 12.

a.,b. Loss of $0.87 mn.

c. Gain of $0.08 mn.

9

Original

Now

∆C

∆r

Total

Ex.8

Ex.9

Ex.11

(9)-(8)-(11)

(9)-(8)

Unhedged port.

$10.00

$8.97

($0.88)

($0.15)

($1.03)

Hedge

($5.69)

($5.44)

$0.01

$0.24

$0.25

Total

$4.31

$3.53

($0.87)

$0.08

($0.78)

10